Tax law in the U.S. can be extremely friendly to real estate investors. Rental property owners can deduct normal operating expenses, and use depreciation to reduce taxable net income. Another benefit of owning rental real estate is deducting travel expenses.

However, there’s a right way and a wrong way to claim travel expenses on your tax return. In this article, we’ll explain how rental property travel expenses work, along with some of the most common travel expense deductions for real estate investors. After all, tax deductions are often seen as one of the biggest benefits of owning real estate.

Note: this is not tax advice and we recommend you speak with your CPA to understand your specific situation.

Can Landlords Deduct Travel Expenses?

Landlords can deduct travel expenses when traveling to visit a remote real estate investment in another market and for going to a property you own locally.

However, the IRS knows that travel expenses are one of the most abused deductions for business people, so it’s important to play by the rules before claiming a deduction for rental property travel expenses.

IRS and Travel Expense Deductions

According to IRS Publication 527, Residential Rental Property:

“You can deduct the ordinary and necessary expenses of traveling away from home if the primary purpose of the trip is to collect rental income or to manage, conserve, or maintain your rental property. You must properly allocate your expenses between rental and nonrental activities. You can’t deduct the cost of traveling away from home if the primary purpose of the trip is to improve the property. The cost of improvements is recovered by taking depreciation.”

The IRS also provides additional guidance for travel expense deductions in Publication 463.

Travel Expense Rules of Thumb

If you’re ever in doubt about whether a specific travel expense is deductible, it’s always a good idea to get professional advice from your accountant or CPA. With that in mind, here are some rules of thumb to follow to help understand if an expense incurred when traveling can be deducted on your tax return:

- Purpose of travel must be mainly for business and have a clear business purpose.

- Majority of the travel time must be spent on your rental business rather than leisure.

- Travel expenses must be “ordinary and necessary” for your real estate business but not overdone, such as staying in a 5-star resort versus an Airbnb or VRBO when going out of town.

- Rental activity like showing the property to prospective tenants or doing an inspection is also a deductible travel expense, provided that was the main reason for traveling.

- Traveling to conduct repairs and maintenance is deductible, but traveling to the property to make a capital improvement such as replacing the HVAC or installing a new roof is not a deductible expense.

Common Rental Property Travel Expense Deductions

Your travel expenses and the reason for taking a trip must have a logical connection to your rental property business.

A good way to decide whether or not a travel expense is legitimate is to use common sense. For example, if your wife or partner says something along the lines of, “Wow, I didn’t know this was deductible!” you may want to think twice before claiming the travel expense.

Now, let’s take a look at some of the common rental property travel expense deductions real estate investors can claim:

- Expenses traveling to and from the airport, such as a taxi or Uber.

- Airfare, train, or bus fare.

- Car rental expenses and associated costs such as parking fees or tolls.

- Travel to a Home Depot or Lowes to shop for materials and supplies to be used for your rental property.

- Traveling to the property to show it to prospective tenants.

- Travel expenses incurred to interview or meet with members of your local real estate team, such as an accountant, attorney, leasing agent, property manager, lender, or general contractor.

- Costs of traveling to an event or meeting for continuing education purposes, such as a seminar, trade show, or convention.

- Shipping costs for luggage or items required for your rental property business.

- Lodging expenses and 50% of meal and beverage expenses incurred while you are traveling outside of your home market.

- Tips paid for service in conjunction with travel to your rental property.

- Miscellaneous expenses such as laundry and dry cleaning, groceries, computer rental fees, or internet charges.

Travel Expenses to a New Rental Market

A recent post on the Stessa blog explains how travel expenses are treated differently when going to a new market to investigate potential rental property to invest in.

For example, let’s say you’ve been researching the Austin real estate market on the internet and know it’s one of the best cities to invest in real estate this year.

If you travel to Austin, incur $2,000 in travel expenses, and eventually buy your first rental property in the market, those travel expenses are not immediately deductible. Instead, they must be capitalized by adding them to your property basis and depreciated over 27.5 years rather than being expensed the year they are incurred.

Now, assume your first rental property in Austin performs beyond your wildest expectations and you want to buy another. This time your travel expenses can be fully deducted (instead of capitalized) because you already own a property in the market, assuming the travel expenses are ordinary and necessary for your rental property business in the market.

So what happens if you travel to a different city to research potential rental properties, but decide not to invest?

In a situation like this, the travel costs are considered a business start-up expense and can only be deducted after you buy your first rental property in that market. If you’re a remote real estate investor, it may be a good idea to research as much as possible online. Then, wait to travel to the market once you have a property under contract and the home has passed its preliminary inspections.

How Auto Deductions Work

Real estate investors who own rental property in their home market can claim the auto expense deduction provided by the IRS.

As a side note, your home market – also known as your “tax home” – is your regular place of business. For most real estate investors, the home market is also the city that they live in. Even if you own rental property remotely, or in an area of the country outside of your home market, you still do the majority of your work on your rental property business from your home office.

There are two ways rental property owners can claim an auto expense deduction:

Standard Mileage Deduction

The standard mileage deduction is the easiest way to claim an auto deduction when traveling to a rental property in your own market. To calculate the mileage deduction, simply keep track of your miles driven for your rental property business and multiply by the standard mileage rate.

The standard mileage rate issued by the IRS for 2021 for a car, van, pickup, or panel truck is 56 cents per mile. For example, if you drove a total of 500 miles this month for rental property-related purposes, the standard mileage deduction would be $280 (500 miles x 56 cents).

Actual Expense Deduction

The second way that rental property investors can claim an auto expense is by keeping track of all auto expenses and business-related miles, then claiming proportional share used for business as the actual auto expense deduction.

For example, assume your auto expenses – items such as car payments, gas and oil, insurance, repairs and maintenance, car washes, registration and license fees, and tolls and parking costs – were $975 this month. If you drove a total of 2,100 miles and 500 of those miles were related to your rental property business, your actual auto expense deduction would be $232:

- $975 total auto expenses / 2,100 total miles driven = 46.4 cents per mile

- 500 miles related to rental property business x 46.4 cents = $232

Keeping Track of Your Miles

Both the standard mileage deduction method and the actual expense deduction method require you to keep track of the miles driven for your rental property business:

- Odometer reading at the beginning of the period (usually the month or year).

- Odometer reading at the end of the period.

- For each business trip, the date and purpose of each trip, the number of miles driven, and the location of the tip.

Mixing Business with Pleasure

Sometimes it’s possible to mix personal and business travel provided that you do it strategically. Generally speaking, as long as at least 50% of your travel days were spent on your rental property business, your trip may still be tax-deductible

Of course, any lodging and meal expenses incurred on non-business days are not tax-deductible as a travel expense, nor are the travel expenses for a spouse, partner, or child unless they accompanied you on the trip for a legitimate business purpose.

How to Track Rental Property Travel Expenses

You can keep track of your mileage using a logbook or digitally.

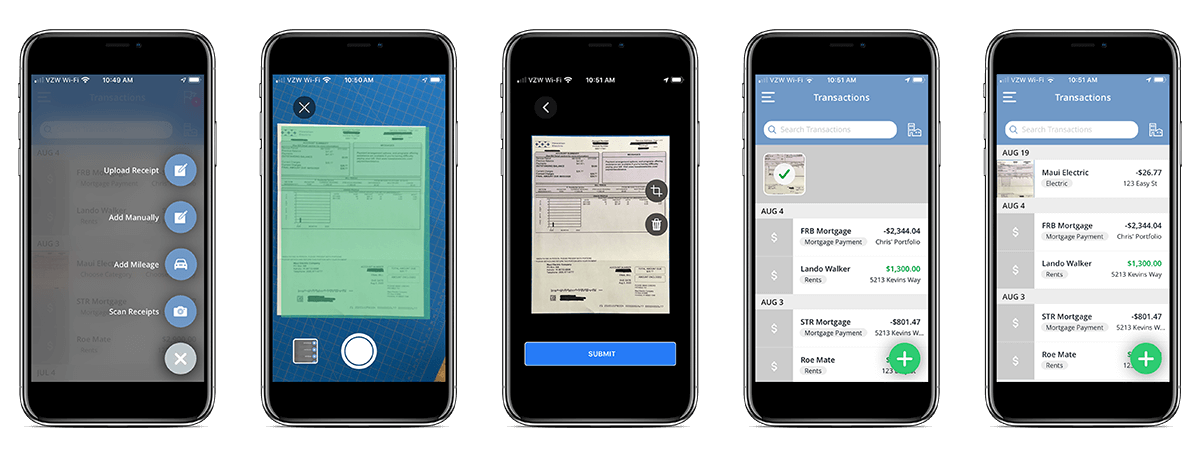

But an even easier way to do this with Stessa’s mobile app. Each time you incur an auto expense, scan the receipt or invoice. Stessa’s machine learning and OCR technologies will parse all of the details and automatically organize the information for you.

Stessa helps streamline the record-keeping process so you can stay organized, maximize your tax deductions, and make informed decisions.

You also get features that make the day-to-day management of your properties easier, including:

- Automated income and expense tracking: Instantly sort and classify transactions from linked bank, lender, credit card, and property management accounts, all without additional fees or required add-ons.

- Financial reporting: Generate income statements, net cash flow summaries, and balance sheets (available with the paid Pro plan), among other reports.

- Landlord banking: Open an FDIC-insured high-yield bank account* for each property and easily integrate them with Stessa’s financial tracking features.

- Rental applications and tenant screening: Use Stessa’s tenant screening services and free rental applications to find and select qualified tenants.

- eSigning (in partnership with DocuSign): Upload your document, tag it for digital signatures, and send it to tenants, vendors, partners, and others.

- Free rent collection: Collect rent from tenants through one-time or recurring ACH payments.

- Real-time performance metrics: Get round-the-clock insights into the performance of your property portfolio.

- Property management integration: Link your property management data portal to Stessa to import transactions and get a detailed portfolio overview.

- Unlimited properties: Add an unlimited number of properties to your Stessa account.

- Collaborative access: Invite other investors, CPAs, spouses, and others to share your Stessa account. Manage their access levels to view and/or edit the account.

- Tax resources: Access the yearly Tax Guide and a suite of educational materials created in partnership with The Real Estate CPA to make tax season a breeze.

Experience a more efficient, stress-free way to manage your rental properties. Sign up for a free account with Stessa today.