While there are various potential benefits to owning rental property, real estate investing can often require a large amount of money. Let’s look at the actual costs of a rental property and explain one cost that is actually a tax write-off real estate investors can use to reduce taxable net income.

Key takeaways

- Several costs determine how much a rental property is, including one-time expenses like a down payment and recurring expenses.

- Rental income collected from a tenant will generally pay for operating costs and the monthly mortgage payment if the property is purchased using financing.

- Depreciation is a noncash expense used by real estate investors to reduce pretax net income.

Costs of owning a rental property: Upfront and recurring expenses to know

There are several one-time, up-front costs and recurring expenses that come with owning a rental property. Here are some of the most common costs to understand before beginning the search for a rental home.

Down payment

There are significant differences between financing a rental property and getting a mortgage for a primary residence. The biggest is the down payment. The down payment for a rental property is generally between 20% and 25% of the purchase price. So, if a single-family rental (SFR) has a sale price of $150,000, the down payment would be $30,000 to $37,500.

While it may be possible to finance a rental property with a lower down payment, real estate investors and lenders typically look for a loan-to-value (LTV) ratio of no more than 80%. If the value of an SFR is $150,000 and the loan amount is $112,500, the LTV would be 75% ($112,500 / $150,000).

A lower LTV may increase the odds of qualifying for an investment property loan because the home has more equity, and the monthly mortgage payment is lower. A lower mortgage payment also increases the cash flow available for operating expenses and contributions to a capital expense (CapEx) account for major repairs or unexpected vacancies.

Closing costs

Closing costs on a rental property generally run between 2% and 5% of the loan amount and are the fees and expenses paid to close escrow and transfer ownership. For example, suppose the loan amount on a rental property is $112,500. In that case, closing costs will run between $2,250 and $5,625, plus the down payment amount.

Typical closing costs to expect when buying a rental property include:

- Loan origination fee for processing loan documents

- Credit report fee

- Loan underwriting fee to assess a borrower's creditworthiness

- Property appraisal to determine if the purchase price is equal to or less than the fair market value

- Property inspection to discover potential problems that may affect property value

- Title search to discover unrecorded liens that may interfere with a borrower’s ownership interest, such as an unpaid contractor

- Discount points or mortgage fees paid to a lender in exchange for a lower interest rate, with one discount point equal to 1% of the mortgage amount

- Miscellaneous fees, such as recording fees, attorney fees, and transfer taxes

- Reserve account of up to 6 months' worth of mortgage payments and operating expenses or as required by lender

Mortgage payment

Interest rates on rental property loans typically are 0.75% to 1% higher than mortgage interest rates for a primary residence, based on factors including a borrower’s credit score, income, and the type of property financed.

For example, if a $150,000 SFR is purchased with a 25% down payment at an interest rate of 6%, the mortgage payment (principal and interest) would be $674 per month. Mortgage payment amounts also include the premium for landlord insurance, property taxes, and homeowners association (HOA) fees. However, these charges are usually itemized on the profit and loss (P&L) report to meet the Internal Revenue Service (IRS) reporting requirements of Schedule E (Form 1040).

Rental property mortgage rates from third-party providers, available through the Roofstock platform, are a good resource for estimating the monthly payment on an investment property. In addition, borrowers can view different scenarios based on loan terms and down payment amount and connect with a lending provider to get preapproved for a rental property loan online. Getting preapproved helps to determine buying power and makes an offer stronger.

Operating expenses

Rental property operating expenses are those necessary for managing, conserving, and maintaining a rental property. While operating expenses are different for every property, here are some of the most common costs to budget for with an SFR or small multifamily building:

- Marketing and advertising

- Tenant screening

- Leasing fees

- Property management fees

- Repairs and maintenance

- Supplies

- Landscaping

- Pest control

- Utilities (sometimes paid by a landlord for a multifamily rental property)

- Landlord insurance

- Property taxes

- HOA fees

- Professional service fees

Suppose a home has never been used as a rental. In that case, real estate investors often use the 50% Rule to estimate operating expenses. According to the 50% Rule, operating expenses should be no more than one-half of gross rental income. For example, suppose a home generates an annual rental income of $18,000. In that case, operating expenses (excluding the mortgage payment) should be a maximum of $9,000 per year.

Another good way to determine operating expenses is by shopping for a rental property on Roofstock. Each home listed for sale includes a breakdown of expenses and due diligence items, such as a preinspection report, title report, and tenant rent ledger if the house is currently rented.

Depreciation

Depreciation is another cost of owning a rental property. However, unlike the expenses discussed so far that reduce cash flow, depreciation is a noncash expense used to reduce pretax net income.

Rental property depreciation is a tax write-off provided by the IRS to compensate real estate investors for property wear and tear, deterioration, and obsolescence. Unlike commercial property, which has a much longer depreciation schedule, residential investment property is depreciated over 27.5 years.

To calculate depreciation, begin by determining the cost basis of the rental property. Next, subtract the land or lot value from the home's purchase price, then add closing costs that must be capitalized, such as recording fees and owner's title insurance. The final number is the cost basis for depreciation purposes and is divided by 27.5 to calculate the annual depreciation expense.

To illustrate, assume that the purchase price of an SFR home is $150,000, including a lot value of $15,000. If capitalized closing costs are $2,000, the cost basis would be $137,000 and the annual depreciation expense would be $4,982:

- $150,000 purchase price - $15,000 lot value + $2,000 capitalized closing costs = $137,000 cost basis

- $137,000 cost basis / 27.5 years = $4,982 annual depreciation expense

The above example shows how depreciation works with rental property. But keeping track of rental property depreciation can be much more complicated in real life. That's why tens of thousands of investors have already signed up for a free account with Stessa.

Free rental property software from Stessa automatically keeps track of depreciation and updates the real estate balance sheet. After linking bank accounts and the mortgage account, income and expenses are automatically tracked, and owners can monitor property performance in real time from a single, comprehensive online dashboard.

Income taxes

Depreciation expenses can significantly impact the amount of income taxes an investor pays. In fact, rental property depreciation is a reason some investors report little or no taxable net income while still having positive cash flow.

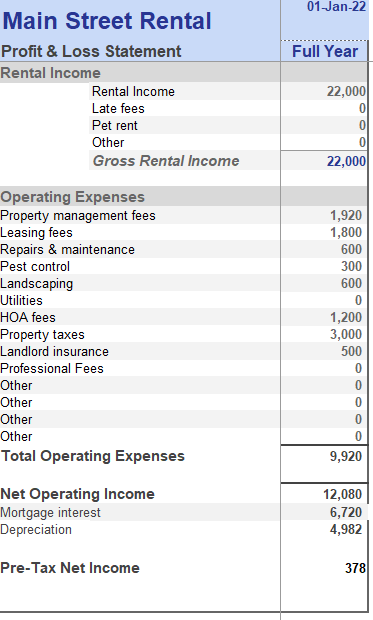

The following graphic illustrates how rental property depreciation can reduce pretax net income:

After collecting the monthly rent and paying operating expenses, mortgage interest and depreciation expense are subtracted to determine pretax net income. Even though the rental property in this example has a positive net operating income (NOI) of $12,080, pretax income is reduced to just $378 after subtracting mortgage interest and depreciation expense.

One of the many benefits of owning rental property is how the income it generates is taxed. In most cases, the IRS considers rental property income “passive income,” which means income is not subject to withholding taxes like Social Security, Medicare, and unemployment tax. Instead, rental income is taxed based on an investor’s federal tax bracket without having to withhold payroll taxes.

Final thoughts

The cost of rental property includes 2 types of expenses.

First, there are one-time, up-front expenses, such as the down payment and closing costs if a property is financed. Then, there are recurring operating expenses, such as property management fees, repairs and maintenance, landlord insurance and property taxes, HOA fees, and the monthly mortgage payment.

Rental income collected from a tenant will generally cover the expenses of owning and operating a rental property. However, it's still important to keep funds in reserve to cover unexpected expenses.