In a report released earlier this year, the National Association of Realtors (NAR) noted how capitalization rates (aka cap rates) across all asset classes have been consistently trending downward over the past 10 years. When you think about it, it’s easy to understand why low cap rates are quickly becoming the norm.

Income-producing real estate is the only asset that offers the trifecta of recurring cash flow, a low correlation to the potentially wild gyrations of the stock market, and inflation-adjusted appreciation over the long term.

Experienced investors know that a trend can be your friend. In this article, we’ll discuss why many investors prefer to buy low cap rate investment properties.

Cap Rate Overview

Let’s begin by taking a look at how the cap rate formula is used to value income-producing real estate:

- Cap Rate = NOI (net operating income) / Property Value

So, a rental property with an NOI of $12,000 per year – which is calculated by taking rental income and subtracting expenses (excluding the mortgage payment and non-cash expenses such as depreciation) – in a 5% cap rate market would be valued at $240,000:

- $12,000 NOI / 5% cap rate = $240,000 property value

In the real world of real estate investing, cap rates are more nuanced and complex than the above examples indicate. That’s because we’re dealing with cash flows that can and do fluctuate from a physical asset such as real estate over the entire holding period.

A cap rate is based on two variables:

- Expected return (or required rate of return) that you expect to receive during the time you hold the investment. This is what the 5% cap rate in the above example represents.

- Growth rate of income (NOI) that you expect to receive over your holding period. However, while your required rate of return may not change over time, your NOI can. For example, unexpectedly long periods of vacancy, higher than expected repair or capital improvement costs, and annual rent increases all affect NOI in negative and positive ways.

In low cap rate markets, where population and job growth keep increasing, NOI is normally more predictable. Stable NOIs mean there is less risk for investors, which in turn increases the demand for rental property. This increased demand also helps to avoid the large swings in property value prevalent in many high cap rate markets.

The Benefits of a Low Cap Rate

The demand for residential rental property is at all-time highs, and will likely stay that way for quite some time. Millennials prefer to rent, and baby boomers do too. In fact, in smaller secondary markets such as Rochester, New York and Athens, Georgia, there is a higher percentage of renter-occupied households than people who own their home.

While many investors complain about not being able to find property with high cap rates, they overlook the key benefits of buying a rental property with a low cap rate:

- Safe returns drive cap rates lower

U.S. 10-year Treasury notes today yield less than 1%, due to the safety and security that government bonds provide. Low cap rate real estate works in a similar way. The reason that cap rates are low in so many real estate markets is because investor sentiment is bullish.

In other words, people are willing to pay more for NOI in a safe and stable market rather than put their investment capital at risk.

- Easier to add value by increasing NOI

For example, raising rents by $50 per month in a 5% cap rate market increases property value by $12,000 ($50 x 12 = $600 / .05 = $12,000). In an 8% cap rate market, the same rental increase only creates a $7,500 value gain.

Everything else being equal, increasing NOI leads to much larger growth in property value and equity in a low cap rate market.

- Low cap rates are a store of value

Investors who buy low cap rate property aren’t typically as much concerned with cash flow as they are protecting their existing wealth. If you don’t count yourself in this category, you’ll be able to by purchasing a property with a low cap rate.

As we’ve seen above, adding incremental value in a low cap rate market exponentially increases the property’s market value, which can result in very impressive gains when and if you decide to sell.

- Smooth exit strategy

A growing number of buyers are looking for the safety and security that real estate investments provide, and it’s likely that the demand for stable returns will continue for quite some time.

Investing in a low cap rate property today will help you to attract more and better-qualified buyers when the time comes to sell.

.jpg?width=2163&name=iStock-1176080337%20(1).jpg)

What is a Good Cap Rate?

A good cap rate for you might be a bad cap rate for another investor, and vice versa. That’s because your investment strategy and tolerance for risk and reward are different from every other investor.

However, you can determine what a good cap rate is by comparing a rental property you’re thinking about buying to alternative investment options and the relative safety they offer.

We noted earlier that the 10-year Treasury bond currently yields less than 1%. Using that rate of return as your risk-free investment option, you may decide that a good cap rate is 5%, provided that the rental property and the real estate market has a relatively low and acceptable level of risk.

How do you know what a low-risk real estate investment looks like? There are several factors to consider to help explain why cap rates are lower in some markets than in other markets with a potentially higher level of risk:

- Geographic Location: diversity of industry and companies, job and population growth rates, education levels, median household incomes, increase in property values, suburban vs. urban neighborhoods, and primary vs. secondary markets.

- Asset Type: residential rental property is generally less affected by an economic downturn, compared to other real estate asset classes such as retail, office, hotels, and industrial property.

- Liquidity: Government-sponsored loans from Freddie Mac and Fannie Mae, along with conventional loans and alternative loans are all generally easier and less expensive to obtain in real estate markets that are stable and predictable.

High vs. Low: Two Cap Rate Examples

To illustrate how a lower cap rate property might actually be a better deal, let’s look at two examples.

Both rental properties are priced the same, and are purchased with the same down payment amount. However, because lenders view the property with the higher cap rate as having higher risk, the loan interest rate is higher on the high cap rate property, even though the NOI is greater:

|

Property #1 |

Property #2 |

|

|

$250,000 at 5% cap rate |

$250,000 at 6% cap rate |

|

|

NOI |

$12,500 |

$15,000 |

|

Loan Amount |

$175,000 |

$175,000 |

|

Down Payment |

$75,000 |

$75,000 |

|

Interest Rate |

4% |

7% |

|

Mortgage P&I |

$10,026/yr |

$13,971/yr |

|

Income |

$2,474 |

$1,029 |

|

Equity Return |

3.29% |

1.37% |

As we can see, even though Property #2 has a higher cap rate and NOI, the equity return – which is calculated by dividing the income received by the down payment – only offers a potential return a little bit higher than a 10-year Treasury bond, but with much more risk. On the other hand, Property #1 with a 5% cap rate generates about 4X the return than a government bond currently does.

Other Financial Metrics to Know

In addition to the cap rate calculation, real estate investors also use several other financial metrics to help determine whether or not a rental property is a good investment:

Gross rental income

Gross rental income is the total income collected before any expenses are paid, including items such as fees for late rent payment and miscellaneous income such as extra pet rent.

Cash flow

Cash flow is the money left over at the end of each month, after all of the bills, including the mortgage, have been paid.

Cash-on-cash return

Cash-on-cash return compares the cash invested to the cash received and is another name for equity return. If you make a down payment of $50,000 and receive an annual net cash return of $10,000 your cash-on-cash return is 20%:

- $10,000 Cash Received / $50,000 Cash Invested = 0.20 or 20% Cash-on-Cash Return

Net operating income (NOI)

NOI is calculated by subtracting your gross income from your normal operating expenses. Net operating income is different from cash-on-cash return, since NOI does not include a deduction for your mortgage payment.

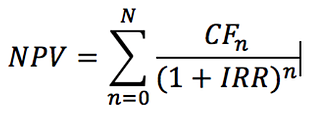

Internal rate of return (IRR)

IRR uses the time value of money and opportunity costs concepts to measure the profitability of an investment over your anticipated holding period:

As you can see, the formula for calculating IRR can be complex. You can easily calculate the potential IRR – along with many other financial metrics – of any property with this simple spreadsheet by Roofstock.

Gross rent multiplier (GRM)

GRM is a quick and easy way to determine the potential value of a property and is calculated by dividing the property purchase price by the gross annual rental income:

- $150,000 Property Price / $12,000 Gross Annual Rents = 12.5 GRM

Generally speaking, the lower the GRM the more attractive the investment could be, everything else being equal.

Loan to value ratio (LTV)

LTV is used to measure the leverage used to purchase a property, and is calculated by dividing the loan amount to the property value:

- $105,000 Loan Amount / $150,000 Property Value = 0.70 or 70%

Normally investors will use conservative leverage of between 60% - 75% when financing a rental property.

Final Thoughts

As a rule of thumb, properties with low cap rates are perceived as having a lower risk level, more predictable cash flow streams, and a greater potential for appreciation.

Although many investors shy away from them, the safety and stable returns from low cap rate properties can create significant opportunities for the buy-and-hold real estate investor.