Homes in many markets are still selling quickly after being listed, and often with multiple offers. The median days on market is 53.5 as of December 2021, according to the Federal Reserve, a number that’s been trending downward over the past several years.

A good property can sometimes be hard to find, and the last thing a buyer wants to do is lose the home to another investor. In this article, we’ll look at 7 steps to follow to make an offer on a property, what to include in an offer, and important contract terms every buyer should know.

Key takeaways

- Before making an offer on a property, a buyer should obtain a mortgage preapproval to help make an offer stronger.

- Key steps for making an offer on a property include locating the best real estate markets for rental property, determining an offer price, reviewing possible contingencies to include in an offer, and presenting an offer to the seller.

- Important contingencies a buyer may include in an offer include appraisal, property inspection, and review of tenant documents if the property is already rented.

- A seller may accept an offer or submit a counteroffer to the buyer.

- Once a buyer and seller agree to all terms and conditions, the offer is signed and escrow is opened.

7 steps to make an offer on a property

Here’s an overview of how to make an offer on a property.

1. Get a mortgage preapproval

A mortgage preapproval is similar to a test drive for an actual mortgage. After reviewing a borrower’s credit and income information, a lender will provide details such as the maximum mortgage a borrower is approved for, along with interest rate and closing cost estimates.

The preapproval letter proves to a seller that a buyer can afford to purchase the home, and it should be included with the offer.

2. Shop around for an investment property

Once a buyer knows the maximum amount that can be financed, it’s time to shop around for a property. Buyers looking for a primary residence often use a local real estate agent or online listing services like Zillow or Realtor.com.

However, investors who want a property already occupied by a renter, or a place that’s rent-ready, are likely to be more successful on the Roofstock Marketplace. Both long-term and short-term single-family and small multifamily properties are listed for sale, oftentimes already rented to a tenant.

3. Determine the offer price for the rental

While a preapproval letter indicates how much home a buyer can afford, that’s not necessarily how much a buyer should spend. To determine the offer price for a rental property, an investor should analyze factors such as job and population growth in a market, the number of homes occupied by renters and rent price growth, sales comparables of similar properties in the same area, and projected return on investment (ROI).

This simple spreadsheet by Roofstock provides an easy way to view the potential financial performance of a given property. You can use it to forecast the potential return of a property. Simply enter some information to view projected key return on investment (ROI) metrics, including cash flow, cash-on-cash return, net operating income, and cap rate.

4. Review contingencies

Contingencies in an offer are things that must occur in order for the transaction to move forward, such as a property appraising for the purchase price, a buyer qualifying for financing, or approving a home inspection report. A contingency can protect a buyer and usually allows the earnest money deposit to be returned if the transaction falls through.

Sometimes a buyer will decide to waive a contingency, such as the financing contingency if a cash offer is being made, or a home inspection in an ultra-competitive market. However, before doing so, a buyer may wish to consult with a real estate agent or attorney to understand the potential consequences of waiving contingencies.

5. Submit a written offer

Once an offer price has been determined and contingencies have been reviewed, the next step is to submit a written offer to the seller.

An offer includes proposed terms and conditions of the transaction, including purchase price, financing, contingencies required by a buyer, closing date, and the deadline for a seller to accept the offer.

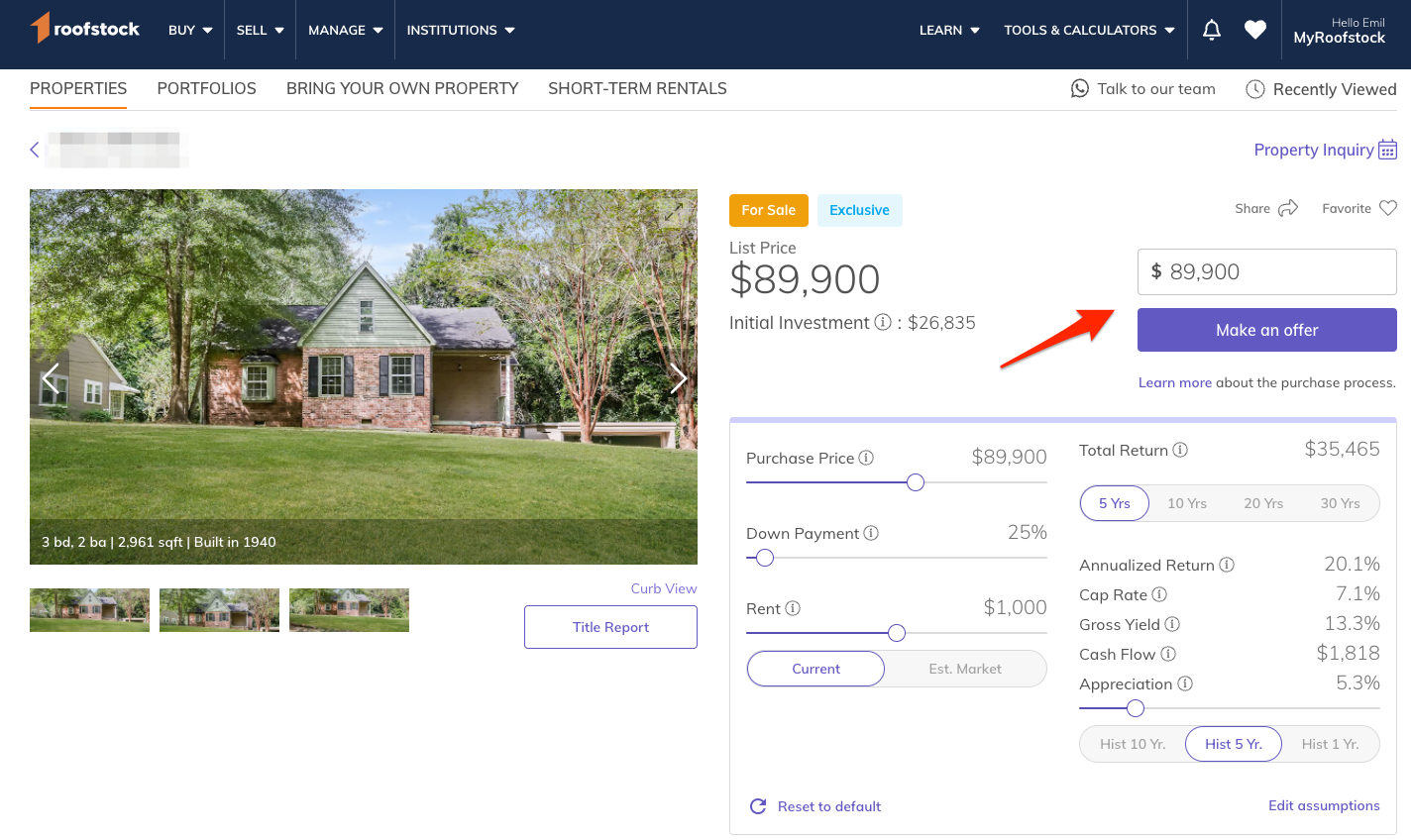

Making an offer for a property listed on Roofstock is even easier. The entire transaction can be done completely online, simplifying the process for remote investing in rental property.

Offers are free to submit, and Roofstock charges a fee of just 0.5% of the contract price or $500, whichever is greater. Properties may have much of the due diligence done, such as title reports and property inspections (when available).

6. Negotiate the purchase and sale agreement

When a seller agrees to all terms and conditions, the offer becomes legally binding once the seller signs and returns the agreement to the buyer or buyer’s agent. However, there will be times when a seller doesn’t agree and will submit a counteroffer to the buyer with different terms and conditions than those originally requested.

If a buyer agrees to a seller’s counteroffer, the document is signed and escrow is opened. Or, a buyer can counter a seller’s counteroffer with different terms and conditions. In some cases, negotiations can go through several rounds of counteroffering back and forth.

During the time that an offer is being negotiated, it’s possible for a buyer to have second thoughts and withdraw from the negotiation or for a seller to accept an offer from another buyer.

7. Finalize the contract and open escrow

Once a buyer and seller have come to a meeting of the minds, the offer (along with any counteroffer) is signed and escrow is opened with a title company or real estate attorney, depending on state law. Earnest money is deposited, the lender begins the mortgage process and orders an appraisal, and the buyer begins inspections.

What to include in an offer

Depending on the state in which a property is located, an “offer” may also be known as a “purchase offer” or a “residential real estate purchase and sale agreement.”

The terms and conditions contained in an offer may vary based on both state and local laws. Some states require a real estate attorney to prepare an offer, while others allow a licensed real estate agent to draw up an offer on behalf of a buyer.

Some buyers prefer to submit a nonbinding letter as an offer to “test the waters” with a seller. The risk of doing this is that, during negotiations, the property may be sold to another investor. That’s why, as a rule of thumb, a buyer or agent will give a seller a complete written real estate purchase agreement with a deadline for acceptance.

An offer to purchase a property generally includes these basic terms:

- Property address and legal description

- Purchase price, including total amount paid, down payment amount if the property is financed, or if the transaction is all cash

- Earnest money, based on a flat fee or percentage of the purchase price, and what happens with the earnest money when the contract is accepted or the transaction is terminated

- Requirement for a seller to deliver “clear” title

- Closing costs and fees, and how the charges will be split between buyer and seller

- Seller disclosures of known issues, lead-based paint, and homeowner association (HOA) information

- Contingencies such as buyer financing and loan approval, property inspection, and property appraising for at least the purchase price

- Specific date of closing

- Date and time a seller has to accept or counteroffer before the buyer’s original offer expires

Understanding contingencies and disclosures

A contract contingency is something that must occur for the transaction to move forward and to close, such as the property appraising for at least the purchase price or a buyer approving an inspection report.

A disclosure is generally something that a seller must tell a buyer, such as any known property defects or the existence of an HOA. A buyer may also be required to disclose certain items to a seller, such as something that may prohibit the buyer from closing on the transaction, like a pending bankruptcy or divorce.

Local and state laws may differ on the specific contingencies and disclosures required in an offer on a property. Here are some of the most common ones for buyers and sellers to be aware of.

Contingencies

- Appraisal of the property for at least the purchase price, often ordered by a buyer even if the purchase is all cash

- Property inspection, including any repairs requested by a buyer, when they will be done, and who will pay for them

- Final loan approval with terms and conditions acceptable to the buyer, such as interest rate and closing costs

- Review of rent roll and tenant documents if the property is occupied by a renter

- Sale of a buyer’s existing property that must occur prior to the transaction closing

Disclosures

- Lead-based paint disclosure if the property was built before 1978

- Disclosure of other potential health hazards, such as asbestos or radon gas

- Nuisances in the neighborhood, including noises from a nearby freeway or airplane overflight, smoke and odors, or proximity to a hazardous waste site

- Recent repairs made, known structural damage such as roof problems or foundation settlement, termite infestation (past or present), and water damage that could cause mold growth

- HOA information, including rules and regulations, dues and fees, meeting notes, current profit and loss, balance sheet, and any known pending assessments

- Number of insurance claims made by the seller in the last 5 years, which may affect a buyer’s ability to obtain a new homeowner or landlord insurance policy

- Death in home, normally other than from natural causes, such as a murder or suicide

- Prior use of the property as a drug manufacturing facility

Final thoughts

Once an offer on a rental property has been accepted, closing can occur in as few as 30 days. During that time, an investor may conduct inspections, review information on the tenant if the home is already rented, and visit the property in person. Other tasks an investor may do prior to closing include opening business banking accounts, setting up an limited liability company (LLC), and signing up for a free account with Stessa to track and optimize rental property performance.