Understanding rental yield is one of the keys to successfully investing in real estate. Although some investors believe that the higher the rental yield the better investment the property is, that isn’t necessarily true.

Keep reading to learn how to calculate rental property yield, why bigger isn’t always better when it comes to yield, and how to find homes with a higher rental yield.

Key takeaways

- There are two types of rental yield to understand: gross and net.

- Gross rental yield measures potential return on investment without factoring in operating expenses.

- Net rental yield is another name for cap rate, and takes into account the normal operating costs of a rental property when measuring yield.

- A rental yield that is above market may present an attractive investment opportunity or may be a red flag that the property should be avoided.

What is rental yield?

Rental yield measures the amount of cash generated from an investment property each year compared to the cost or value of the property. There are two types of rental yield in real estate, and both are expressed as a percentage:

- Gross rental yield

- Net rental yield

Both types of yield measure the return on investment from a rental property, but in different ways.

Gross yield is calculated before making deductions for operating expenses. On the other hand, net rental yield (also known as the capitalization rate or cap rate) measures the return from a rental property after deducting operating expenses.

Real estate investors calculate rental yield for two main reasons.

First, both gross and net rental yield help an investor to understand if a property being considered for purchase offers a sufficient return based on the investment strategy.

Secondly, an investor keeps an eye on rental yield to monitor the financial performance of each property held in a real estate portfolio to identify homes that are over or under performing.

How to calculate rental yield

Let’s assume an investor owns a single-family rental home with a market value of $150,000. The rent is $1,500 per month and the operating expenses average 48% of the annual rental income, excluding the mortgage payment and capital expenses.

Gross rental yield calculation

Both types of rental yield measure return on investment on an annual basis. The first step an investor must take to calculate gross rental yield is to convert the monthly rental income to an annual figure, then then divide the annual rental income by the property value:

- Annual rental income = $1,500 monthly rent x 12 months = $18,000

- Gross rental yield = $18,000 annual rental income / $150,000 property value = 0.12 or 12%

Net rental yield calculation

Net rental yield measures the return on investment based on the net operating income (NOI) the rental property is generating.

NOI is calculated by subtracting operating expenses (excluding the mortgage payment principal and interest, capital expenses, and the non-cash deduction for depreciation) from the property’s annual rental income. Net operating income is then divided by the property value to determine the net rental yield:

- Operating expenses = $18,000 annual rental income x 48% average annual operating expenses = $8,640

- NOI = $18,000 annual rental income - $8,640 operating expenses = $9,360

- Net rental yield = $9,360 NOI / $150,000 property value = 0.0624 or 6.24%

Free tools to determine rental yield

Even though rental yield can be calculated by hand, there are two tools real estate investors use to measure the rental yield of a property currently owned and to forecast the potential yield of a rental property being considered for investment.

For your existing portfolio

Investors who already own rental property can sign up for a free account with Stessa, a property management software system designed to make tracking real estate investments simple.

It takes just a few minutes to create an account, to enter basic property information, and to link bank and mortgage accounts. Investors can use Stessa to automate income and expense tracking, generate financial reports, and monitor rental property performance in real time.

One of the unique features of Stessa is that property value in the asset section of the real estate balance sheet is periodically adjusted to current market conditions. With these updates, investors may be able to calculate a rental yield that more accurately measures returns.

For properties you’re evaluating

Stessa is a great option for determining rental yield of a property that’s already owned by the investor. But what happens if an investor doesn’t know the fair market rent and net operating income for the property?

This simple spreadsheet by Roofstock provides an easy way to view the potential financial performance of a given property. You can use it to forecast the potential return of a property. Simply enter some information to view projected key return on investment (ROI) metrics, including cash flow, cash-on-cash return, net operating income, and cap rate.

What is a good rental yield?

Some investors might “ballpark” or approximate a good net rental yield as being around 6% or 7%, while others might say that the higher the rental yield is the better.

However, understanding what a good rental yield in real estate is more nuanced than simply throwing out a number. That’s because rental yield is affected by a variety of other factors, such as the balance between risk and reward.

Some real estate investors are willing to take on more risk than others in exchange for the hope of gaining a bigger reward. To illustrate, we’ll consider a real estate market where the net rental yield on a typical single-family home is around 6%.

If an investor spots a home for sale offering a net rental yield of about 8%, it could mean several things. For example, the home could be priced below the fair market value, which would make the rental yield higher:

- $9,360 NOI / $120,000 priced below market value = 7.80%

- $9,360 NOI / $150,000 fair market value = 6.24%

However, before jumping at the potential opportunity, savvy investors assess whether there are issues with the property that would lower the purchase price, such as a significant amount of deferred maintenance. After making any needed repairs, the new owner could end up with a home that generates a much lower rental yield than anticipated.

Or, the property could be in good condition but the rents are above market, which would also make the rental yield higher than other similar properties:

- $12,360 NOI from above market rent / $150,000 property value = 8.24%

- $9,360 NOI from fair market rent / $150,000 property value = 6.24%

In a situation where the rent is too high, the potential risk to a buyer is that the tenant will leave when the lease is up, and the home would need to be leased to a new tenant at the true market rent. If this occurs, the rental yield will go down, assuming the property value did not change.

Where to find rental homes where the rental yield is already estimated

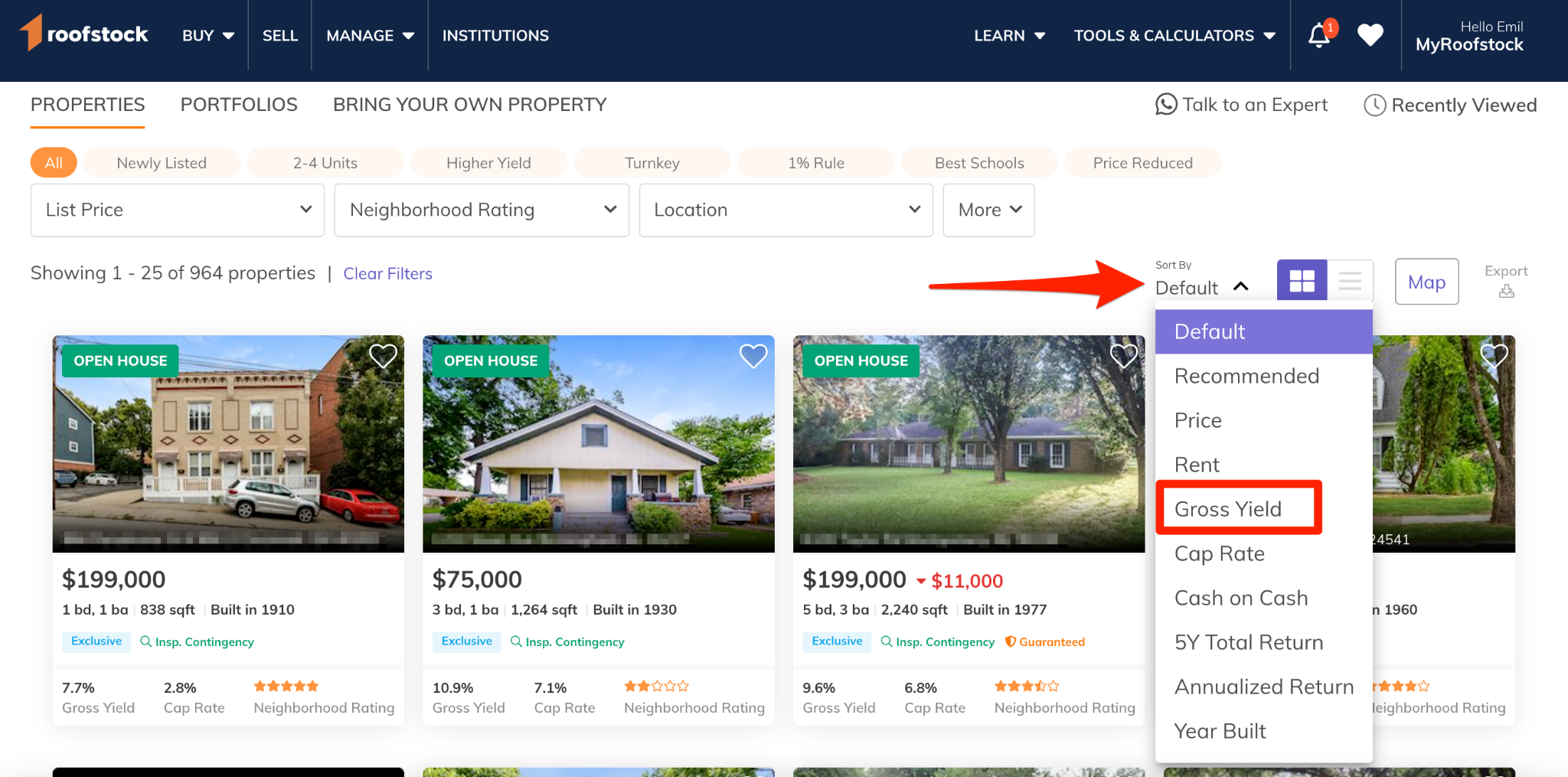

For remote real estate investors looking for affordable rental property in attractive markets with estimated rental yield already calculated, one option is to use the Roofstock Marketplace.

In fact, you can even sort properties based on their estimated gross yield:

Investors can narrow down the search even more from there. For example, by using the neighborhood rating, an investor can find higher yielding homes in the top-rated neighborhoods.

The location selection can be used to search for homes with a higher rental yield in real estate markets in the Midwest and Sun Belt. States such as Ohio and Texas are home to secondary and tertiary real estate markets where job and population growth are pushing rent prices on single-family homes higher.

Tips for increasing rental yield

There are several things an investor can do to help increase rental yield if the property is underperforming compared to similar homes in the same area:

- Ensure that the tenant is charged a fair market rent.

- Make renovations to justify a higher rent, attract higher-quality tenants, reduce operating expenses, and increase property value such as repainting, installing energy-efficient appliances, and making the property pet-friendly.

- Use online rental listing and tenant screening services to find the most qualified tenants for a vacant property in the least amount of time to help keep rental income lost to vacancy as low as possible.

- Identify opportunities to generate additional monthly revenue, such as collecting additional rent for pets or roommates, renting appliances to the tenant, and collecting late fees called for in the lease.

Final thoughts

Real estate investors calculate rental yield to estimate the potential return from a new investment, and to monitor the financial performance of property already owned.

In today’s world, safe investments like 10-year Treasury bonds offer yields of around 1.30%, and junk bond ETFs promise yields of less than 5.00%. Investing in rental property may be an attractive option for investors seeking a balanced blend of risk and potential reward by owning a tangible asset like real estate.